Disclaimer:

This article is an independent educational commentary on historical events and financial instruments as depicted in the film The Big Short (2015).

All analysis and explanations are my own and are intended for educational purposes.

The 2008 Market Crash Explained

Why does it matter?

I started paying close attention to economics and policy changes after a recent tariff showdown and what the experts call a Trade War between the United States of America and China. Coincidentally, I happened to watch The Big Short, a 2015 movie about the 2008 market crash. The movie was about a group of people who have recognized patterns in the market and thus, they were able to successfully predict the ongoing market crash and earn from it. However, I found it really challenging to fully comprehend the subjects, and ideas that the movie was discussing, by people who are unfamiliar with financial verbiage and instruments. In this article, I am aiming to address this issue and explain the strategy and financial instruments behind the plot. You will understand that the 2008 market crash was caused by negligence and ignorance fueled by extreme confidence motivated by greed.

What is Shorting?

Just like a book starts with a cover, a movie starts with its title: The Big Short. Shorting in classic terms means betting that the value of assets will depreciate. In general this term is used to describe a strategy when for example a trader borrows a stock from a broker for a $100, it depreciates to $80, then our trader returns it back to the broker, and broker returns him amount for which he lent a stock, which is $100. Therefore, our trader made $20 of profit. However, this is not exactly the situation that happened in the movie. You may wonder: why was the movie called then The Big Short if nobody was borrowing and returning anything, and you will be correct. Although the main characters were not borrowing and returning credit default swaps, which we will discuss later in this article, they were still “shorting” because they were betting that the housing market would go down.

The Housing Market Before the Crash

So what was the housing market composed; against what they were betting? There were two primary financial instruments that were discussed in the movie: Mortgage-Backed Securities, and Collateralized Debt Obligations. A Mortgage-Backed Security(MBS) is a diversified collection of subprime loans. Subprime loans are high risk loans since they are being offered to borrowers with an impaired credit score. They were referred to as NINJA loans which stands for “‘No Income, No Job, and No Assets’” (American Predatory Lending). In order to compensate for the risks associated with those loans, interest rates for those loans were higher. About 80% of all subprime loans were Adjustable Rate Mortgages(ARM) (American Predatory Lending). An ARM is a type of mortgage that has a fixed rate for a short period of time after which it is subject to an adjustment. This amount by which the rate of a mortgage adjusts depends on indices that were tied to the Fed’s rate.

From AAA to BBB-

Those MBSs were combined with other financial instruments and grouped into Collateralized Debt Obligations. A Collateralized Debt Obligation(CDO) is a diversified pool of bonds, mortgages, loans, and other debt obligations that are divided into tranches. Profits from these bonds are obtained from loan payments and their interest rate. These bonds are “sliced” into tranches that differ by ratings based on their creditworthiness that“reflect the issuer’s financial ability to make payments and repay the loan in full at maturity” (Fidelity). In S&P and Fitch rating agencies rating of AAA is considered the strongest, while rating BBB- is considered the weakest.

Shield of Tranches

Highest rated bonds receive profits first, while lowest rated bonds receive profits last. In general, a CDO was sliced into three tranches: junior – lowest rated bonds, mezzanine, and senior – highest rated bonds. For example, a CDO that $100 million in MBS would be sliced like this: $10 million would go in junior tranches at the bottom; $20 million would be mezzanine tranches, which means that they would act as both debt and equity, and $70 million would senior AAA tranches. Thus, this system would allow the two bottom tranches to absorb at most 30% of losses caused in case of their MBSs’ default while protecting senior AAA tranches in a CDO. However, once losses exceed the 30% barrier, the senior tranche becomes exposed to market losses, yet this inequality was compensated by the fact that higher risk tranches were bringing the most yield, following the concept high risk = high reward. A common practice was to wrap CDO tranches into another CDO, creating synthetic CDOs, thus quadrupling yields and losses.

Try for $1.99, Pay $199.99 Later

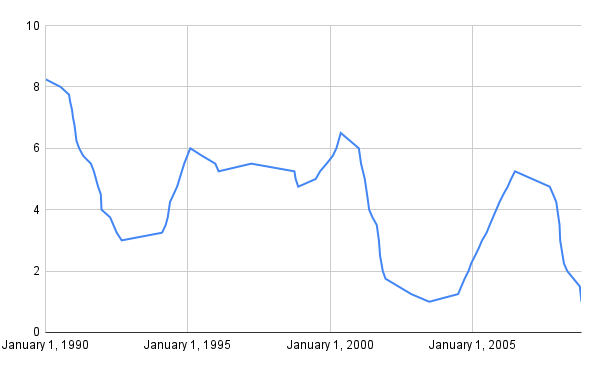

So why did those mortgages default? The answer lies in the fact that those mortgages were ARMs, meaning that their rate was subject to change according to the market. Consider the following scenario a situation where someone took out an ARM in 2003 with a “teaser” rate of 3%. That rate was set to reset in 2006 to be more in line with market conditions. Assume that the loan term is 30 years with a monthly payment of $2,500/month at a 3% rate. According to the formula M=P* r(1+R)n(1+r)n-1 a $2,500/month 3% payment equals a $592,000 loan. So what would happen when the rate resets to 6.5% in 2006? Using the same formula, we can determine that the new monthly payment would be around $3,900/month with 27 years, or 324 months, left, which results in a whopping $1,400/month increase, 56% higher than the original payment. Indeed, around 2006 the Fed’s rate began to rise dramatically, resulting in ARM defaults around the country, which can be seen on the chart with data plotted from fedprimerate.com.

Nothing Ever Happens

If things were that bad, you may wonder, why did nobody do anything about it? The answer to that lies within human greed and bankers’ and investors’ overconfidence in the housing market as a whole. Banks were willing to sell their mortgages in the form of MBSs because it provided them with immediate cash, risk transfer, and fees. Not only it allowed them to transfer the risk and return their money with extra fees, it enabled them to re-lend the money to repeat the cycle again. Similarly, wrapping bad loans into CDOs allowed them to transfer risks from objectively bad and risky loans. Additionally, as I mentioned earlier, rating agencies that were supposed to reasonably rate those loans were financially motivated by banks, so they assigned higher ratings to risky loans. Because these financial instruments were rated as safe and long term, they were purchased by pension funds, foreign investors, insurance companies, etc. They all sought high-yield safe long term returns and they believed that AAA-rated housing market backed instruments would perfectly suffice their goal. Yet, the bankers supposedly knew that those instruments are not reliable, yet their drive for profits encouraged them to continue. Investors who were purchasing those bonds were overly confident in the market and never audited their financial tools.

Somebody’s Loss is Somebody’s Gain

Now it is a good time to discuss how the protagonist of the movie, Michael Burry. He figured how to make money out of it. As we can see in the movie, he realized that the mortgages were about to default soon and around the country. He conducted research during which he found plenty of mortgages with missing payments that were about to default soon. Realizing that, he decided to purchase CDS, or Credit Default Swaps, targeting MBSs and CDOs. A CDS is a financial instrument which is a contract that acts like an insurance against bond default. When a CDS is purchased, a buyer becomes obliged to pay premiums, like for a typical insurance. In return, a buyer receives a payoff if an underlying bond defaults. Additionally, a CDS contract can be successfully bought and sold after it was created, therefore it had a market value. It is important to understand that neither buyer or seller has to own financial instruments that are being insured. So, Burry’s plan was to purchase as many CDSs as they can, and wait for a market collapse soon. We could see in the movie that his fund was losing money for quite a while due to premium payments before the crash happened. When the actual crash happened, it was important for Micheal Burry and others to sell their CDSs while there are buyers who could afford them. One of the biggest insurance firms that was also selling CDSs, AIG, collapsed soon after the market crash because of the amount of defaulted bonds that it had to cover.

Lessons Learned

In conclusion, the 2008 Stock Market Crash was caused by excessive investing in risky financial instruments, such as MBSs and CDOs, that were very likely to default. This happened because the banks were interested in selling bad loans and investors in those financial instruments were overly confident in those instruments. Those who had information about the actual state of those assets bet on their default by buying CDSs that guaranteed to return money if bonds default. Those CDSs had value on their own, so they could be sold if there is demand for them. When the market crashed, the value of the assets plummeted, thus forcing margin calls. Margin calls is a term that describes a situation when the price of a leveraged asset goes down forcing it to lose liquidity. It is a common practice to trade using borrowed money, thus increasing leverage. For example, you have $1 million, which is your liquidity, and you borrow $9 million to buy stocks, bonds, etc., so now you have $10 million worth of financial instruments. In case the market goes 10% down, so you lose $1 million dollars. When this happens, a broker or whoever lent you money makes a margin call that forces the investor to either add more cash (liquidity) or sell assets to cover losses. So, when the actual market collapsed and the prices went down, everyone received a margin call and attempted to sell, but when everyone sold and the prices went down, there was no one to buy, paralyzing the entire market. This has marked a long lasting financial struggle in the United States and around the world.

Resources used:

- Duke University. “Subprime Lending.” American Predatory Lending. predatorylending.duke.edu/business-analysis/evolution-of-mortgage-lending/subprime-lending

- Fidelity Investments. “Understanding Bond Ratings.” Fidelity Learning Center. fidelity.com/learning-center/investment-products/fixed-income-bonds/bond-ratings